Unlike consumer payments, which are focused on individual purchases, B2B payments involve larger sums of money and more complex processes tailored to businesses' needs.

Understand B2B payments if you are looking to streamline your financial operations and improve efficiency. Several payment methods are available for B2B transactions, from traditional checks and wire transfers to modern innovations such as electronic invoicing and virtual cards.

The realm of B2B payments is vast and constantly evolving, so I have created this comprehensive guide to help you navigate the complexities of B2B payment solutions. In this guide, I will cover the basics of B2B payments, explain popular payment types, discuss the importance of payment automation, and analyze the challenges traditional payment methods face. Let’s start!

.webp)

B2B payments are transactions in which businesses exchange goods or services for a particular currency. Although paper checks are still used, digital payment solutions are becoming more popular due to their efficiency in issuing, receiving, and processing payments, ultimately improving cash flow.

B2B transactions are more complicated and time-consuming than B2C transactions, as they require longer approval and settlement times, which can take days or even weeks. Additionally, B2B payments often involve larger sums, necessitating more advanced payment processing systems to manage higher sales volumes and complex remittances.

In summary, B2B payments enable the exchange of value between businesses, requiring robust and efficient payment systems to satisfy the needs of both buyers and sellers.

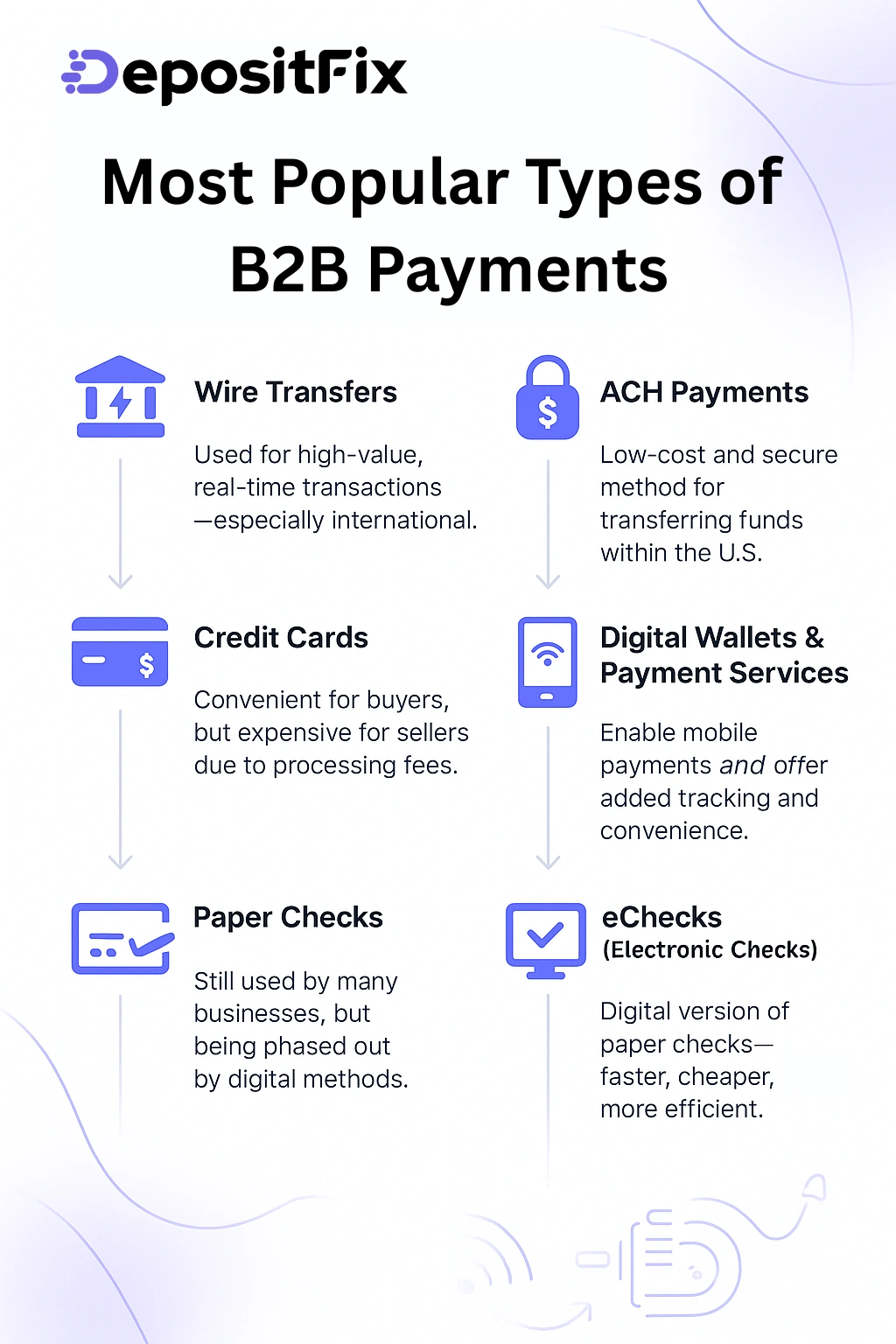

Although wire transfers are not used as frequently as other methods for B2B payments, they still make up a significant portion of the volume, particularly for high-value transactions involving international entities.

Wire transfers are processed through Fedwire, CHIPS, or RTP systems. They ensure immediate funds availability in the recipient's account upon receipt, making them a popular choice for real-time payments.

However, wire transfers can pose security risks and are considered one of the less secure options for B2B transactions.

Automated Clearing House (ACH) payments are an affordable and convenient way to transfer funds electronically within the United States. They are highly secure and widely used in B2B transactions. The ACH network connects all banks in the US, enabling the transfer of funds between accounts held at different financial institutions with minimal friction and communication between parties.

While ACH is possible for international transfers, wire transfers are more commonly used as they bypass intermediary verification. However, ACH payments are still preferred in the US for businesses seeking efficient and secure fund transfers.

Despite the processing fees involved, commercial credit cards remain a preferred payment method for buyers, including businesses. However, accepting credit cards is one of suppliers' most expensive payment methods.

For many businesses, accepting credit card payments is an essential decision. Not doing so can lead to a potential loss of business that far outweighs any immediate cost-saving benefits. Companies can implement strategies such as credit card surcharging to minimize these expenses.

Also, various credit card processing technologies are available in the market that aim to minimize the costs passed on to businesses. These solutions streamline and automate credit card payments, reducing manual tasks, expediting cash flow, boosting revenue, and enabling key team members to focus on strategic initiatives rather than payment processing. This is probably the most widespread method of paying which you can come across on a multi-vendor marketplace platform, eCommerce store, or even when making online donations.

These platforms enable purchasers to make payments for products or services using digital devices. Examples of digital payment services include:

They facilitate the electronic transfer of funds between accounts. Usually, the transfer occurs between two parties and circumvents direct access to bank accounts, although they remain linked.

Specific consumers favor digital wallets and online payment services due to their supplementary functionalities, such as the ability to include a note with a transaction and additional tracking features. The convenience of overseeing transactions via a mobile device also adds to their appeal.

Although the use of paper checks by individual consumers has significantly decreased in recent years, it remains a prevalent payment processing method for businesses. The reasons why many companies continue to use paper checks, other than sticking to outdated practices, are not entirely clear.

However, digital payment methods are undeniably the future of payment processing. The shift towards digitization and the demand for convenience by consumers across different industries has led to a move towards digital B2B payment methods.

Specifically, the adoption of digital B2B payment methods and the digitization of accounts receivable (AR) processes is transforming customer relationships and revolutionizing the collaboration between AR and accounts payable (AP) teams. This transformation is driven by the increased efficiency and transparency that digitization provides.

Electronic or eChecks are processed digitally and contain the same information as traditional paper checks.

So, eChecks offer faster payment processing and lower transaction fees than credit card payments. Sellers benefit from quick and cost-effective transactions, while buyers enjoy the convenience of digital payment.

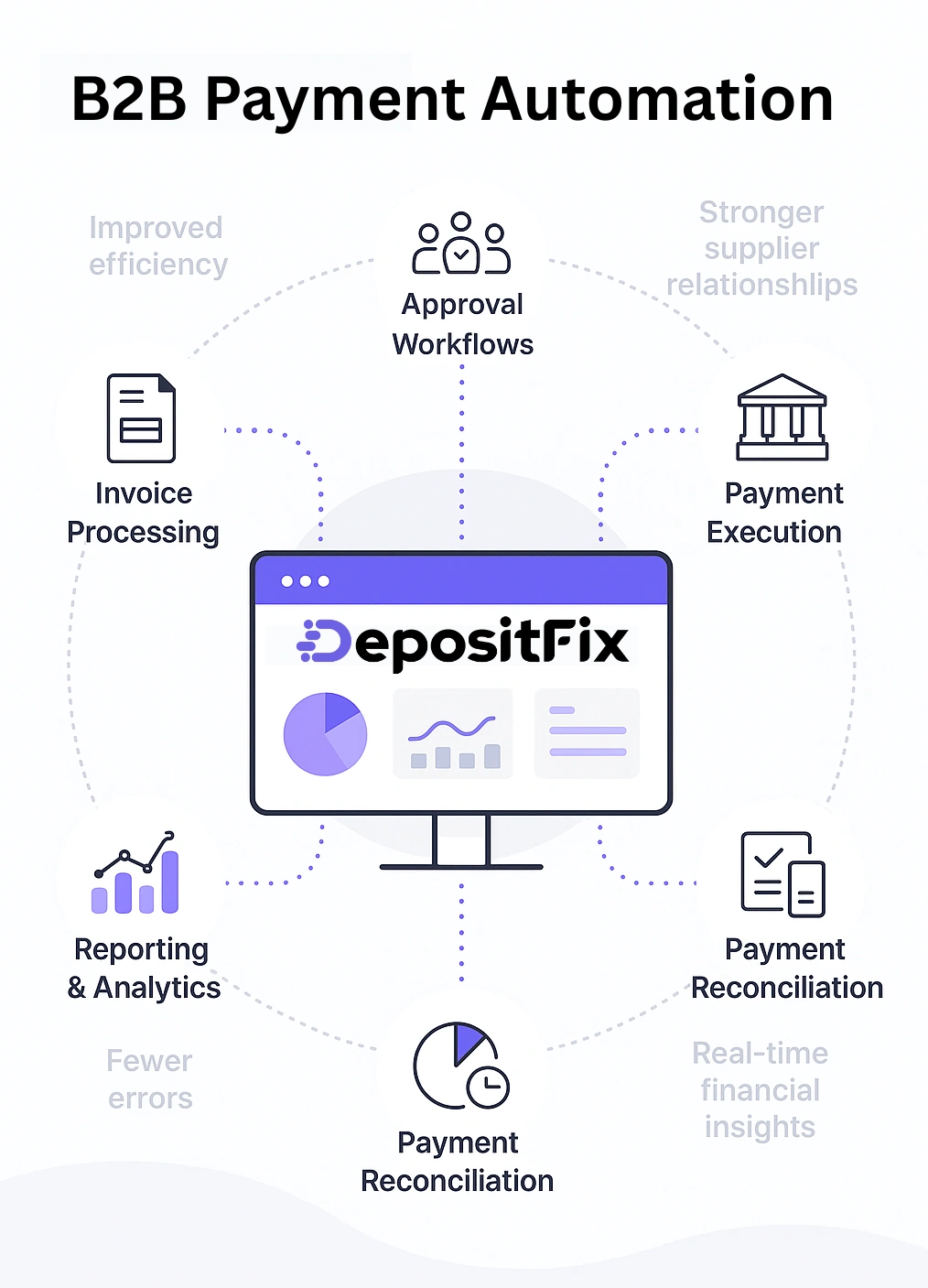

B2B payment automation involves:

Automating these processes can help your business allocate resources more effectively, minimize manual errors, and focus on strategic initiatives.

Use suitable B2B payment automation software to improve efficiency while significantly reducing costs. The benefits extend beyond cost reduction, accuracy, and efficiency.

B2B payment automation can also strengthen supplier relationships, ensure regulatory compliance, mitigate fines and penalties, and provide valuable insights into cash flow and financial well-being.

The process of automating B2B payments involves several key steps, including:

Traditional B2B payment methods create challenges for businesses trying to collaborate with one another. These methods involve manual processes and disconnected systems, which limit flexibility and integration.

They don't work well with ERP systems, don't provide enough payment data for remittance advice, and offer limited transparency. This lack of unified payment data visibility makes it difficult for internal departments and external partners to collaborate effectively. In addition, traditional payment methods don't integrate well with modern digital payment methods, which can create further complications.

They typically only provide basic payment information, such as the amount and date, making it difficult for AR teams to match payments to outstanding invoices promptly.

Payment fraud attacks often target businesses because, due to higher transaction volumes, they can offer more lucrative opportunities for fraudsters. While electronic payments can also be targeted, traditional payment methods provide easier access to sensitive information.

The threat of invoice fraud is increasing, making it imperative for companies to adopt secure B2B payment systems and solutions. Many businesses invest in enhanced security measures such as fraud detection software, cloud consulting services, or dedicated staff for transaction monitoring to reduce fraud risks.

However, these additional security investments can add up quickly, especially for enterprises that engage in a significant volume of B2B transactions.

Traditional payment methods can slow down payment processing times, which can create delays throughout the entire payment process. However, electronic payment methods can speed up payment cycles for both accounts payable and accounts receivable.

Traditional methods can result in time lags in B2B payments that can negatively impact cash flow. For example, checks can take several days or even weeks to process, while wire transfers can also take several days to complete.

Traditional B2B payment methods often result in delayed payments. Factors such as manual processes, payment disputes, inefficient systems, limited visibility, and fund transfer delays can cause this.

Processing checks manually can be costly, error-prone, and time-consuming for AR teams. This makes paper checks a significant obstacle to improving cash flow. Additionally, delivering paper checks by mail takes days, which introduces uncertainty about when payment will be settled.

Customers may take advantage of these inefficiencies to prolong payment delays whenever feasible.

Traditional B2B payment methods, such as wire transfers and paper checks, incur various fees, predominantly borne by the seller, significantly inflating operational costs. These fees encompass processing charges, intermediary costs, and currency conversion fees.

Implementing B2B payment solutions conserves valuable resources such as time and money for the business, its employees, and its customers. With this solution, merchants eliminate the need to physically write checks, deposit them, and reconcile them.

Processing a physical check typically costs $2 per transaction, which can accumulate significantly with a high volume. By leveraging B2B payment solutions, teams can redirect their efforts towards core products and services more efficiently while AI takes care of mundane tasks.

An efficient B2B payment solution can significantly simplify the management of accounts payable and receivable. It eliminates the need for manual handling of numerous checks by autonomously scanning, logging, and archiving them, thereby reducing the likelihood of errors and minimizing human intervention.

This system can seamlessly integrate with ERP, accounting, or bookkeeping software, enabling shared data management and functionality. This integration enhances operational efficiency and simplifies tax filing processes.

Mailing a check puts businesses at risk of payment fraud. Although digital solutions are not entirely immune to security breaches, most payment providers have teams of engineers and experts who work tirelessly to protect your data 24/7.

Also, conducting transactions electronically creates a more transparent "paper trail," which improves accountability and traceability throughout the payment process.

8 in 10 fail within five years due to cash flow problems. Automate your B2B processes instead of relying on paper checks. Doing so lets you gain insights into cash flow patterns, which can help make strategic spending decisions. For small businesses aiming to streamline financial operations and maintain optimal cash flow, leveraging professional financial expertise can make all the difference. Utilizing virtual CFO services for small businesses ensures you have the strategic guidance needed to manage payments efficiently, forecast cash flow, and adapt to evolving market conditions, all while focusing on growth.

Payment software platforms can provide comprehensive reports on accounts payable and receivable, which can help identify timely and delayed payments for proactive management. Additionally, B2B accounting software can streamline payment collection, allowing customers to pay with a click. This can accelerate cash inflow and improve overall financial stability.

.webp)

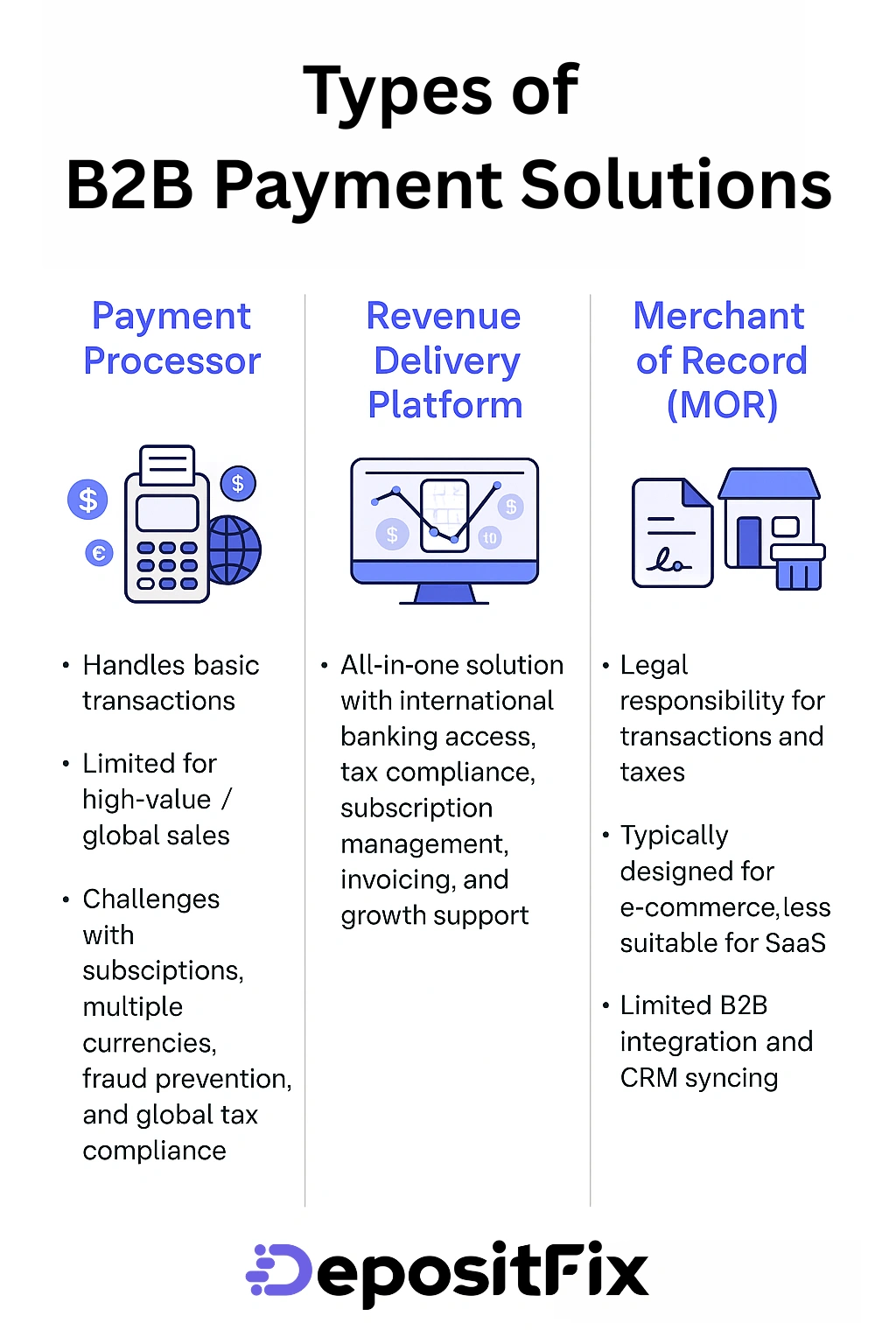

A payment processor is a common method for handling B2B payments, but there may be better options for global SaaS sales. Payment processors often have limitations, such as lower transaction values and unsuitability for higher-value transactions. Additionally, managing self-serve payments introduces complexities such as:

These tools may not be tailored for SaaS companies, leading to payment routing, dunning, and SaaS-specific logic issues. Furthermore, they do not solve the challenge of global sales tax compliance, leaving businesses fully responsible for tax registration, filing, and remittance worldwide. While payment processors may seem cost-effective initially, the cumulative expenses increase when other essential tools in the revenue delivery pipeline are considered.

A revenue delivery platform consolidates various B2B payment processing tasks and tools into a single interface. This platform offers several benefits, such as instant access to international banking infrastructure, which enables streamlined payments across different countries and currencies.

Additionally, it enhances the checkout experience to maximize payment conversions, provides global tax management and compliance integration, offers flexible subscription management for optimized recurring revenue, and centralizes all payment and revenue data. It also includes integrated invoicing for seamless operation and dedicated growth support to navigate the evolving SaaS market.

A Merchant of Record (MOR) refers to the legal entity responsible for selling goods or services, handling transactions, and assuming liability, including sales tax compliance.

However, MOR platforms can be expensive and may not provide robust B2B capabilities. They were initially designed for e-commerce or physical products and may not be entirely suitable for SaaS businesses.

While they offer B2B payment methods, they may not integrate seamlessly with modern billing processes. Additionally, MORs may not be able to bridge the B2B payments gap effectively, as they may not sync with CRM tools, leading to data silos and hindering responsiveness to growth opportunities.

Inefficient financial operations can hinder the profitability and growth of online businesses, posing challenges even for those who have mastered marketing strategies. DepositFix provides a comprehensive payment solution for high-growth companies, addressing common pain points such as fragmented payment data and manual spreadsheet work.

By smoothly integrating with platforms like HubSpot, DepositFix helps businesses:

With a focus on scalability and efficiency, DepositFix empowers businesses to overcome operational hurdles and unlock their full growth potential in today's competitive digital landscape.

Navigate the complexities of B2B payment solutions to optimize your financial operations and drive growth. The landscape of B2B payments is rapidly evolving, encompassing traditional methods like wire transfers and paper checks as well as modern innovations such as digital wallets and electronic checks.

Understand the challenges and trends in B2B payment processing and make informed decisions about adopting automation, integrating with ERP systems, and selecting the right payment solution provider. Embracing digital payment methods not only streamlines processes but also enhances security, improves cash flow, and fosters collaboration between internal departments and external partners.

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!