An ACH Notification of Change (NOC) is a message sent by a receiving bank to alert the originator that incorrect information was used in a recent ACH transaction—such as an outdated account number or bank routing number.

This notification helps ensure future payments are processed smoothly and prompts the originator to update their records with the correct information.

What Is ACH Notification of Change

An ACH Notification of Change (NOC) is a message sent by a Receiving Depository Financial Institution (RDFI) to the Originating Depository Financial Institution (ODFI) to inform them that there is incorrect or outdated information associated with an ACH (Automated Clearing House) payment transaction.

This usually occurs when the transaction was processed successfully but contained data that needs to be updated for future payments, such as a change in the recipient's bank account number, routing number, or account type. Rather than rejecting the transaction altogether, the RDFI allows it to go through and then issues the NOC to ensure that future payments are directed using the corrected information.

The ODFI is then responsible for passing the NOC details to the originator—often a business or organization—who must update their records accordingly. NACHA rules, which govern the ACH network, require that originators make the necessary corrections within a specific timeframe, usually within six business days of receiving the NOC, to prevent delays or errors in subsequent payments.

How Does ACH Notification of Change Work

ACH Notification of Change (NOC) is a process in the U.S. banking system used to notify originators (businesses or individuals sending ACH payments) when there is incorrect or outdated information in an ACH transaction — such as a wrong account number, bank routing number, or account type.

This is how it works:

Transaction with Incorrect Info

An ACH transaction (like direct deposit or bill payment) is sent by the originator but contains incorrect or outdated banking details for the receiver.

RDFI Identifies the Error

The Receiving Depository Financial Institution (RDFI) — the receiver’s bank — accepts the payment but flags the incorrect information.

They still process the payment (so it’s not rejected), but they issue a Notification of Change (NOC) back to the sending bank.

NOC Sent to Originating Bank

The Originating Depository Financial Institution (ODFI) receives the NOC, which contains:

- The incorrect information.

- The correct updated information.

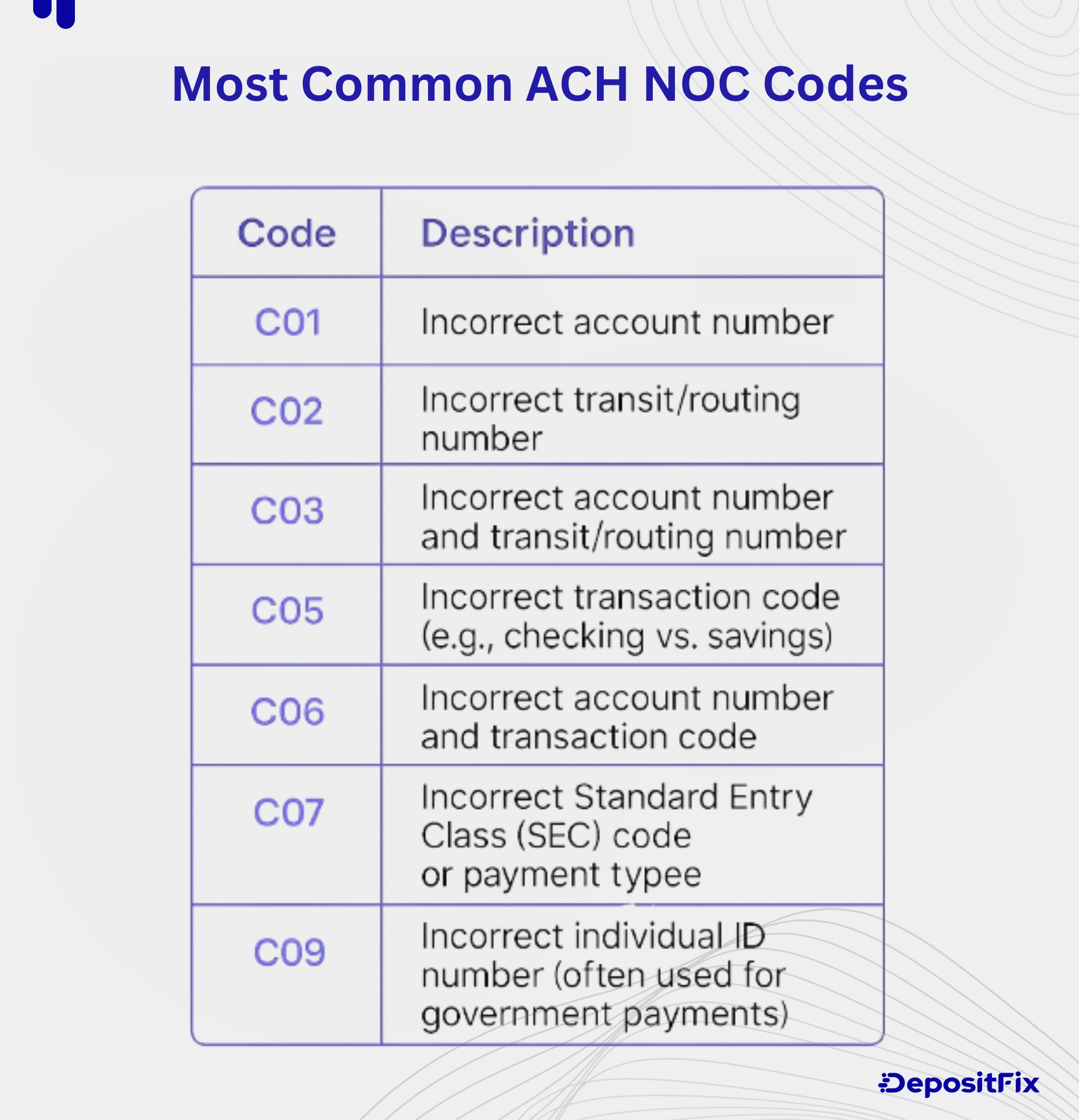

- A Change Code that describes the type of correction needed (e.g., “C01” for incorrect account number).

Originator Must Act

The originator (business or sender) is responsible for updating their records with the correct information within 6 banking days or before the next payment, whichever is sooner.

There are more than 50 different NOC codes, with some of the most common ones listed in the table below.

ACH Return Codes are standardized codes that indicate why an ACH transaction was returned. They help identify issues like insufficient funds or incorrect details.

ACH Payment Returns occur when ACH transfers are rejected or reversed due to issues like insufficient funds, incorrect details, or unauthorized transactions.

Ready to streamline your payment operations?

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!