Business-to-Business ACH (Automated Clearing House) is a fast, secure, and cost-effective method for companies to transfer funds electronically between business bank accounts. Unlike traditional paper checks, B2B ACH payments streamline the payment process and automate transactions, reducing errors, and improving cash flow management.

This system is widely used for vendor payments, payroll, and other recurring business expenses, helping organizations save time and reduce processing costs.

Business-to-Business ACH (Automated Clearing House) refers to the electronic network that facilitates the transfer of funds directly between bank accounts of two businesses.

Unlike consumer ACH payments, which often involve payroll deposits or bill payments, B2B ACH transactions are specifically designed to handle larger payment volumes, higher dollar amounts, and more complex transaction requirements typical of business operations.

This system replaces traditional payment methods like paper checks or wire transfers and enables automated, secure, and efficient movement of money for invoices, vendor payments, supplier settlements, and other commercial transactions.

B2B ACH payments usually follow standardized formats governed by NACHA (the National Automated Clearing House Association), ensuring compliance, consistency, and reliability across the network.

Because these payments are processed in batches through clearing houses, they tend to be more cost-effective than wire transfers, with lower fees and fewer risks of errors or fraud. As a result, many businesses are increasingly adopting B2B ACH payments to improve cash flow, simplify accounting processes, and enhance overall financial management.

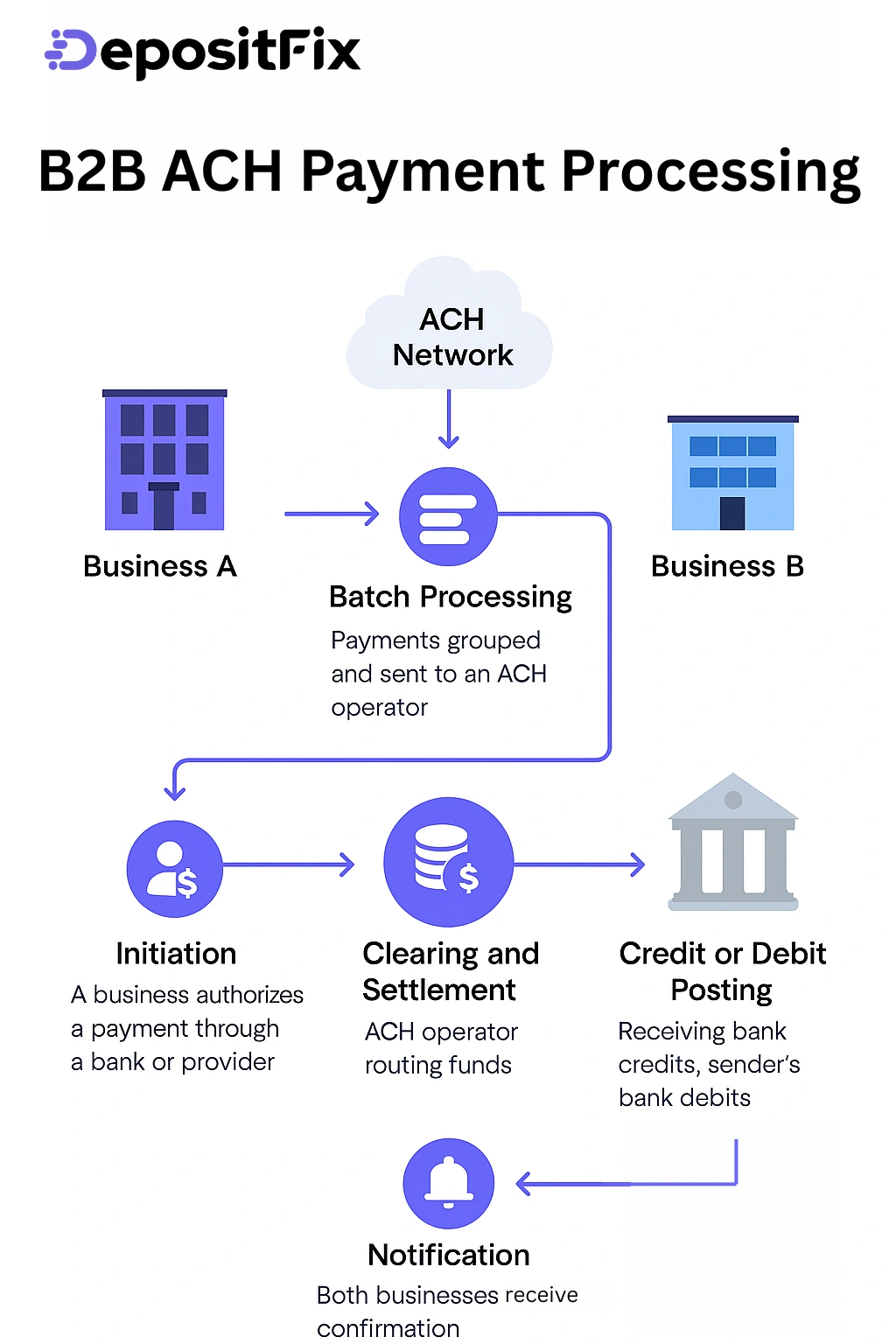

Business-to-Business ACH electronically moves funds between the bank accounts of two companies through the Automated Clearing House network, which acts as a centralized clearing system for batch processing of payments. Here’s how the process typically unfolds:

The paying business (the sender) authorizes a payment to the receiving business (the beneficiary) by submitting payment instructions through their bank or payment service provider. This authorization can come from an invoice approval, a contract, or pre-established payment terms.

Instead of processing transactions individually, ACH payments are collected and grouped into batches by the sending bank. These batches are then sent to an ACH Operator (a central clearing facility), such as the Federal Reserve or the Electronic Payments Network.

The ACH Operator sorts and processes the batches, then routes the payments to the receiving banks. This step verifies funds availability and confirms transaction details.

The receiving bank credits the beneficiary’s account with the payment amount, while the sender’s bank debits the sender’s account accordingly.

Both businesses receive confirmation of the completed transaction through bank statements or payment reports, allowing them to update their accounting records.

Here are the most important benefits of ACH payments compared to other payment methods:

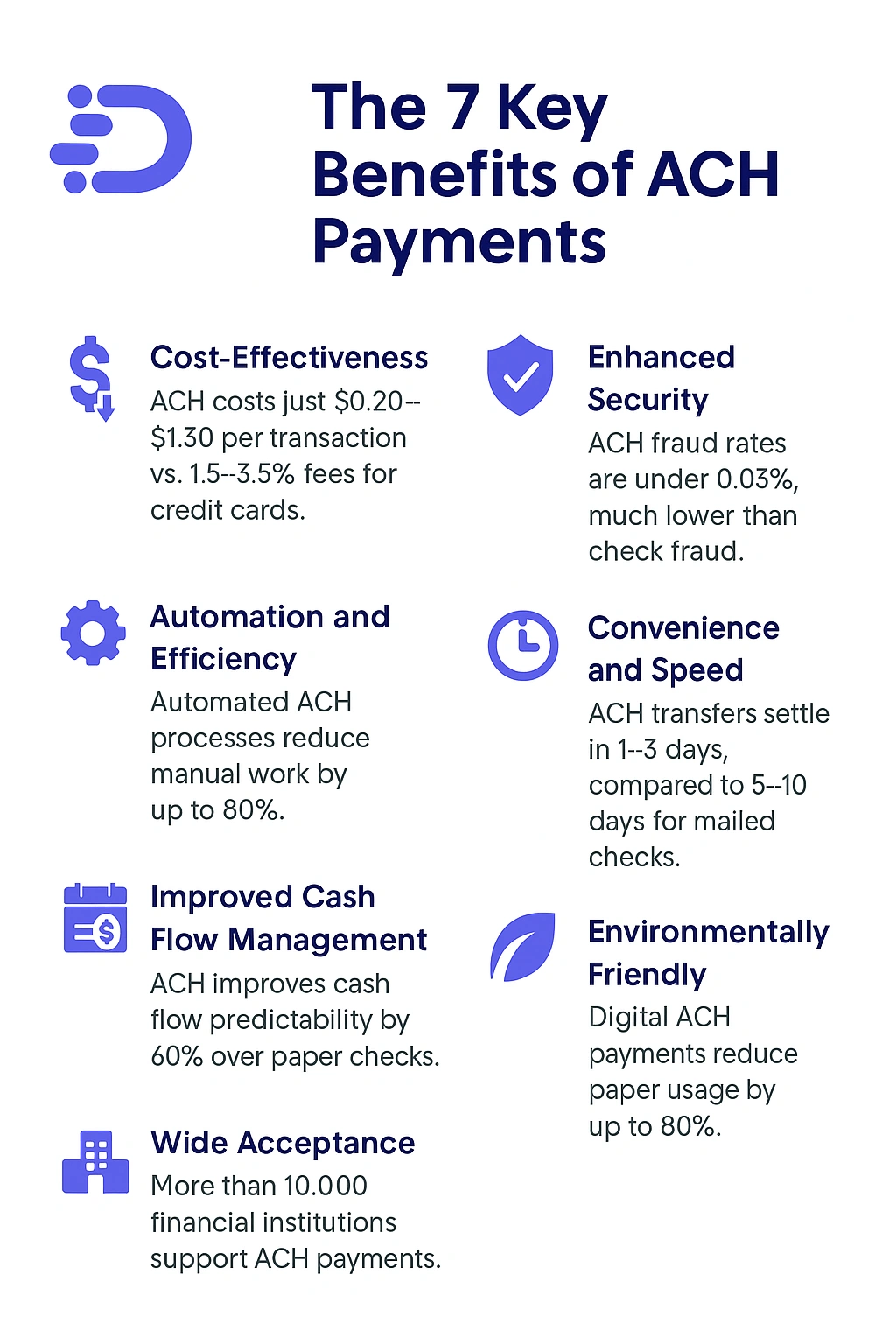

ACH payments typically have lower fees than credit card transactions or wire transfers, helping businesses save money on payment processing costs.

ACH enables automated, scheduled payments that reduce manual work, minimize human errors, and streamline accounts payable and receivable processes.

When businesses schedule payments and receive funds electronically, they can better predict cash flow timing and reduce delays caused by paper checks.

ACH transactions are encrypted and governed by strict banking regulations, making them more secure and less susceptible to fraud than paper checks or cash payments.

While not instant, ACH payments usually settle within one to three business days, which is faster than mailing paper checks and more cost-effective than wire transfers.

ACH payments eliminate the need for physical checks and postage, reduce paper use, and contribute to more sustainable business practices.

Most banks and businesses support ACH transactions, making it a broadly accessible payment method for B2B transactions of all sizes.

Here are some common challenges of Business-to-Business ACH transactions:

ACH payments typically take one to three business days to clear, which can be slower than wire transfers or instant payment methods, potentially delaying cash flow.

Some banks impose limits on the maximum amount per ACH transaction, which may not suit businesses that need to transfer very large sums frequently.

Incorrect account information or authorization issues can cause payments to be returned or rejected, requiring manual intervention and slowing down the process.

Implementing ACH payments requires careful setup, including obtaining proper authorizations, ensuring compliance with NACHA rules, and integrating with banking systems or payment software.

Unlike real-time payment systems, ACH does not provide instant confirmation of payment receipt, which can complicate reconciliation and cash management.

Although secure, ACH payments are still vulnerable to fraud such as account takeover or unauthorized debits, so businesses need strong internal controls and monitoring.

ACH is primarily a U.S.-based network, so it is not suitable for cross-border transactions, requiring alternative payment methods for international B2B payments.

Despite these challenges, many businesses find that the benefits of ACH payments outweigh the drawbacks when proper processes and safeguards are in place.

Here’s a detailed look at the costs associated with accepting Business-to-Business ACH payments:

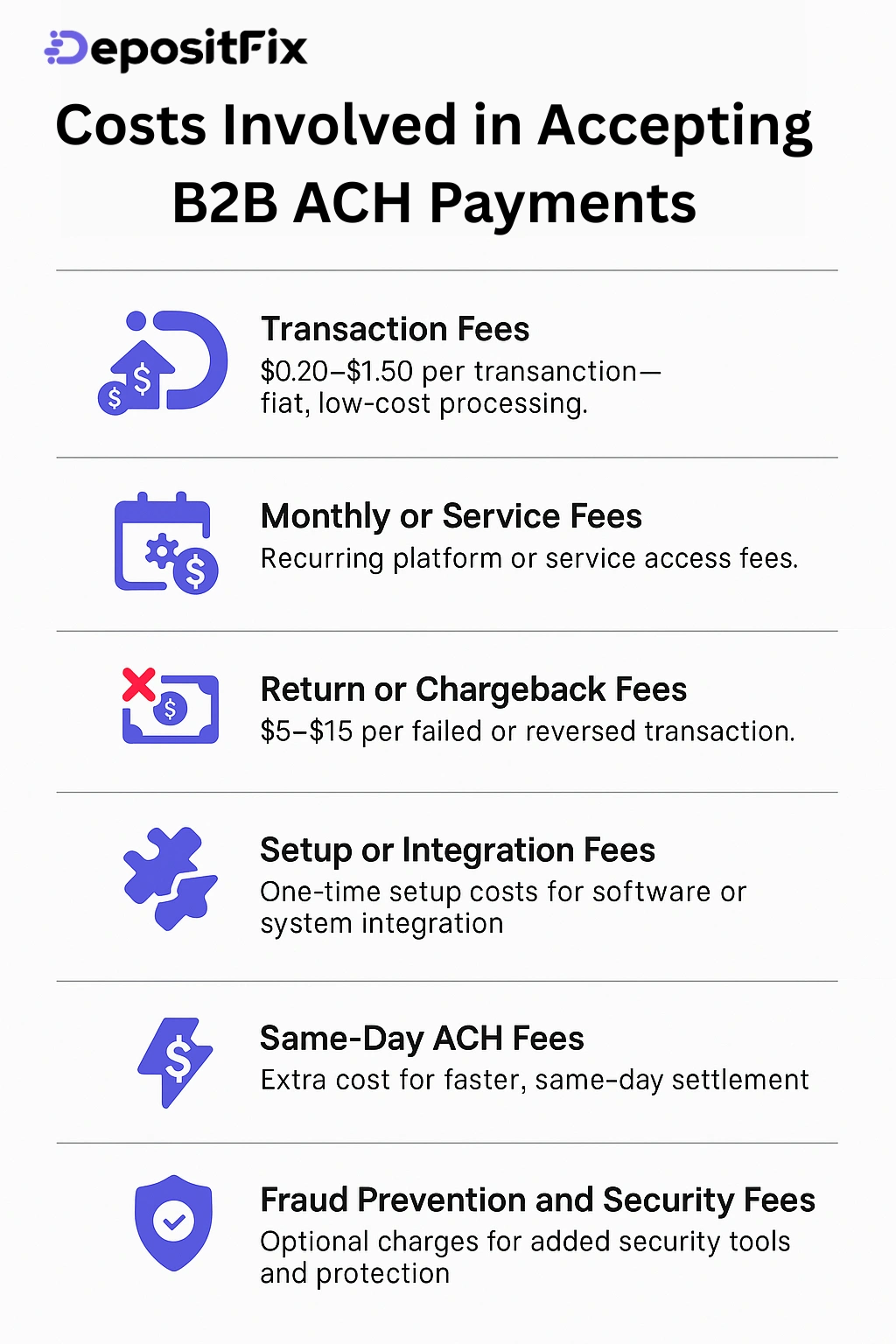

When you accept ACH payments, your bank or payment processor usually charges a per-transaction fee. This fee is typically a flat rate, often ranging from $0.20 to $1.50 per transaction, which is generally much lower than credit card processing fees.

Some providers charge a monthly fee for maintaining ACH payment services or access to their payment platform. This fee covers ongoing support, software access, and network connectivity.

If a payment is returned due to insufficient funds, invalid account numbers, or authorization problems, the receiver (your business) may be charged a returned payment fee, typically between $5 and $15 per incident.

Accepting ACH payments may require initial setup or integration with your existing accounting, billing, or ERP systems. Depending on your provider or software, there could be one-time setup or onboarding fees.

If you want to receive payments faster via same-day ACH, expect to pay a premium fee per transaction compared to standard ACH processing.

Optional services like enhanced fraud detection, tokenization, or encryption might come with additional costs, but they can help protect your business from costly disputes or losses.

Implementing Business-to-Business ACH payments involves several important steps to ensure smooth, secure, and compliant transactions. Here’s a clear guide on how to get started:

Determine the volume and types of payments you expect to process via ACH. Understand your cash flow requirements and identify the benefits ACH can bring to your payment processes.

Select a bank or payment service provider that supports B2B ACH payments and offers competitive fees, robust security features, and integration capabilities with your accounting or ERP systems.

Obtain proper authorization from your business customers to debit or credit their accounts. This typically involves signed ACH authorization forms that comply with NACHA rules to ensure legality and reduce risk.

Work with your payment processor or use payment software to connect ACH capabilities to your billing, invoicing, or ERP platforms. This enables automated initiation and reconciliation of payments.

Educate your finance and accounting teams about the ACH payment workflow, including how to initiate payments, monitor transactions, handle returns, and maintain compliance.

Regularly review ACH transactions for accuracy, timeliness, and fraud prevention. Use reporting tools to track payment performance and optimize your processes.

Start accepting ACH payments effortlessly with DepositFix, a powerful payment solution designed to simplify your B2B transactions.

DepositFix streamlines the entire ACH payment process and seamlessly integrates with your website and accounting systems, allowing you to securely collect payments directly from your clients’ bank accounts.

With DepositFix, you benefit from faster payment processing, reduced transaction fees compared to credit cards, and enhanced cash flow management. Its user-friendly interface and automated workflows minimize manual tasks, reduce errors, and ensure compliance with industry standards.

Whether you’re invoicing vendors, collecting recurring payments, or managing large transfers, DepositFix makes accepting ACH payments straightforward, reliable, and efficient, helping your business get paid faster and with less hassle.

Business-to-Business ACH payments offer a secure, cost-effective, and efficient way for companies to manage their financial transactions. ACH automates the transfer of funds between business bank accounts, reduces manual effort, lowers processing costs, and improves cash flow predictability.

While there are some challenges—such as processing times and setup requirements—the benefits far outweigh these hurdles for most businesses. Implementing ACH payments with trusted partners like DepositFix can further simplify the process, ensuring smooth, reliable transactions that help your business thrive.

Embracing B2B ACH payments is a smart step toward modernizing your payment operations and building stronger financial relationships with your partners.

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!