A running payment is the process of executing payments that have been approved and are ready for disbursement, typically in bulk or as part of a scheduled payment cycle. It involves moving funds from a business's account to its vendors, suppliers, or service providers after all invoice checks and internal approvals are complete.

A running payment refers to the actual execution phase within the accounts payable process, where approved and validated invoices are processed for payment. It involves the systematic transfer of funds from a company’s bank account to its vendors, suppliers, or service providers.

This step typically occurs after all preceding steps, such as invoice matching, validation, and internal approval, have been completed. Running a payment often includes preparing a batch of payments, selecting the payment method (such as bank transfer, check, or digital payment), initiating the transactions, and ensuring that all necessary authorizations and controls are in place. This process may be handled manually or automated through accounting or enterprise financial systems.

A well-run payment process ensures that obligations are met on time, helps maintain healthy supplier relationships, reduces the risk of late fees or service disruptions, and contributes to accurate cash flow management. In essence, running payments is the point where financial commitments are fulfilled, making it a critical function in a company’s financial operations.

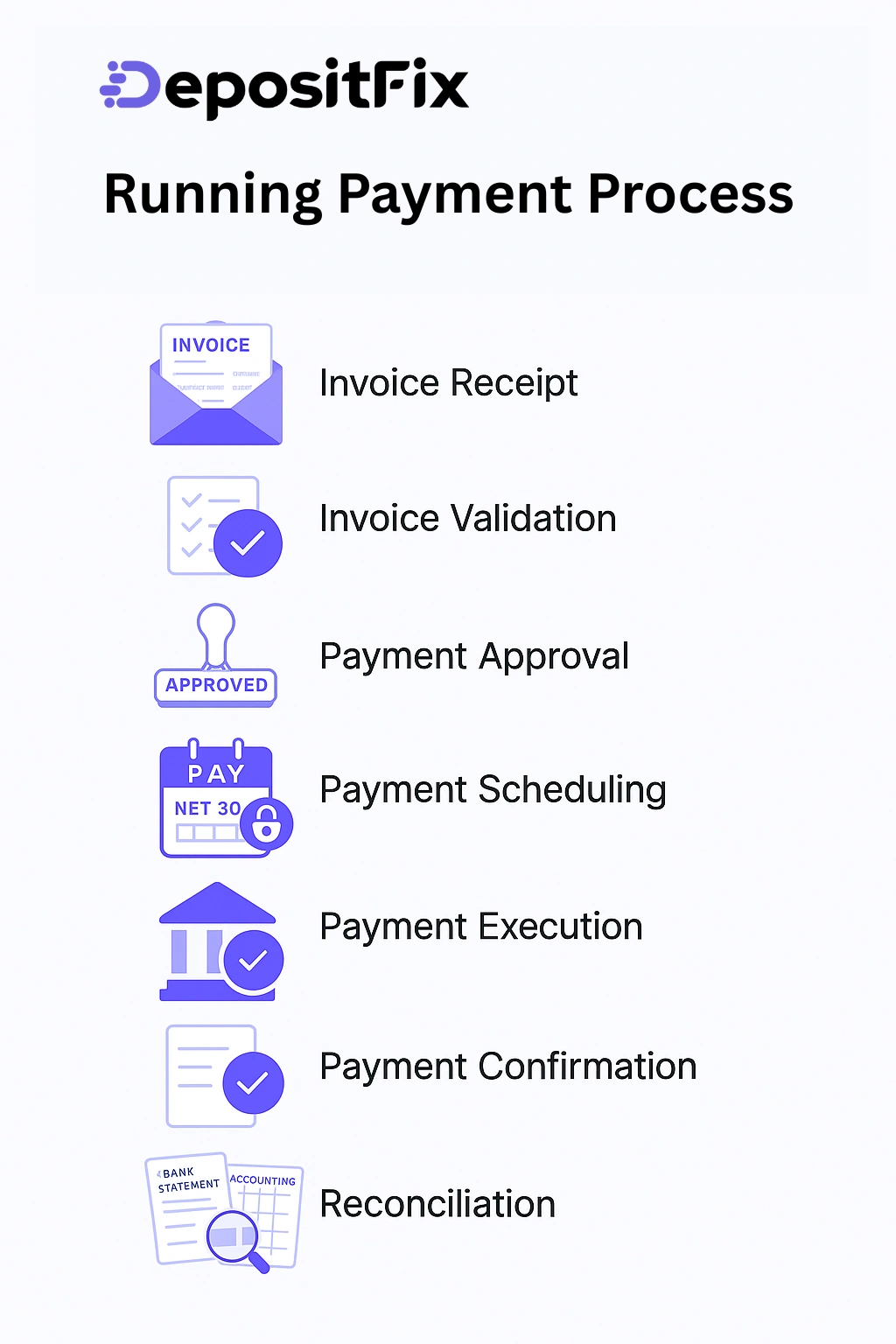

The running payment process refers to the steps a business or system takes to initiate, authorize, and complete a payment, typically for vendor invoices, employee salaries, or other payables. It’s a core part of accounts payable or financial operations and usually includes these stages:

This is the starting point of the payment process. A business receives an invoice from a supplier, contractor, or service provider, which serves as a formal request for payment. Invoices can arrive through various channels, email, postal mail, electronic data interchange (EDI), or uploaded through a vendor portal. The invoice typically includes details such as:

Before an invoice is paid, it must be validated to ensure it’s accurate and legitimate. This step helps prevent fraud and accounting errors. Validation usually involves:

Once validated, the invoice needs internal approval before payment. The approval process varies based on company policy, but often involves:

After approval, invoices are queued for payment. At this stage, the business decides when to pay based on:

This is the core of the payment cycle, when the actual disbursement of funds happens. The process involves:

After payments are executed, confirmation is received from the bank or payment service, indicating which payments were successfully processed. At this stage:

Finally, businesses perform reconciliation to ensure that payments made match the entries in the accounting records. This includes:

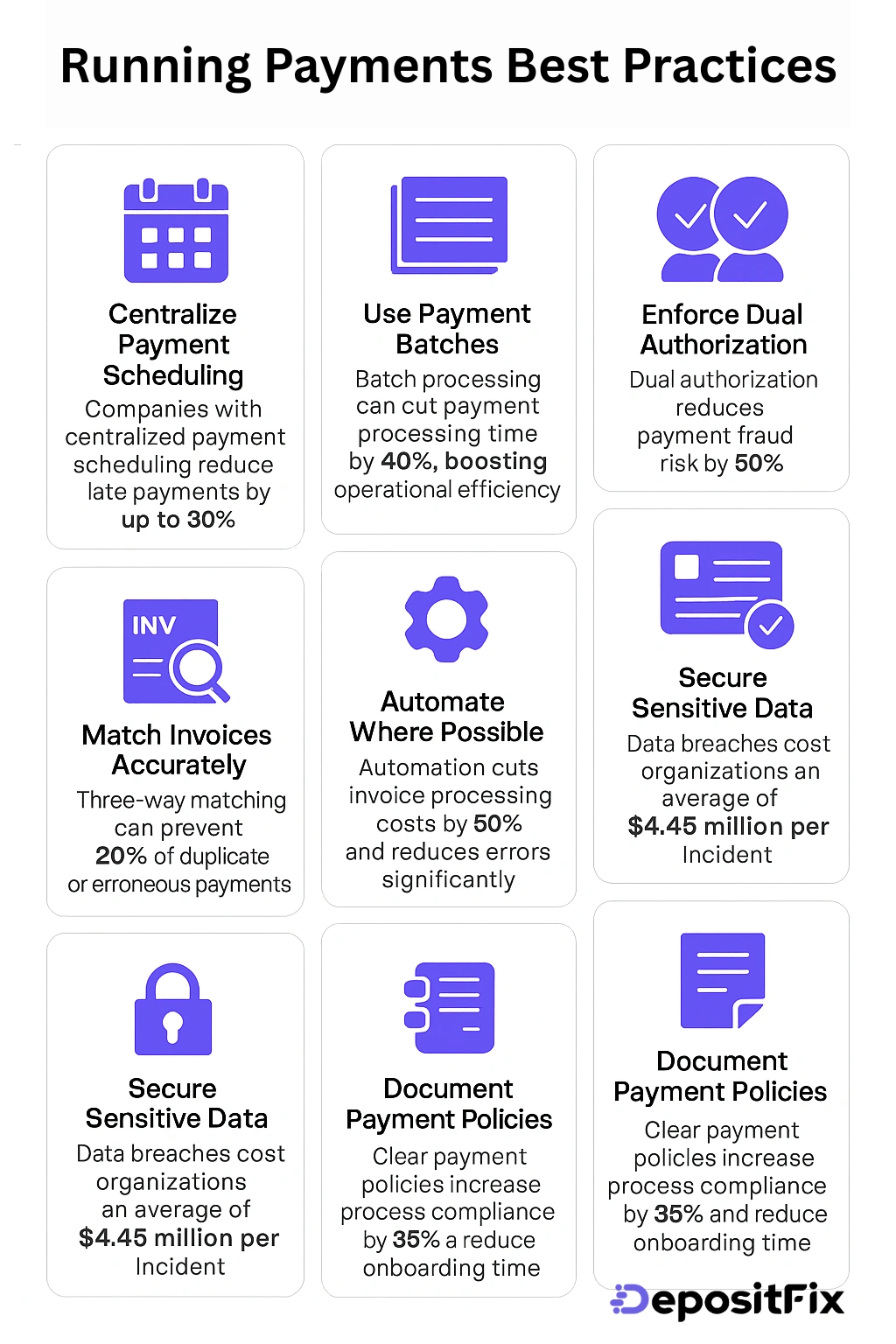

Here are some best practices for running payments that help ensure accuracy, efficiency, and financial control:

Coordinate all payments from a central schedule. This allows better cash flow forecasting, helps avoid missed or duplicate payments, and makes it easier to track due dates and early payment discounts.

Group payments by due date, vendor, currency, or payment method. Running payments in batches improves efficiency and reduces administrative overhead, especially for recurring or high-volume payments.

Implement a dual-approval process for releasing payments, especially large transactions. This internal control helps prevent fraud and errors, as it requires two sets of eyes before funds are released.

Ensure vendor information (e.g., banking details, contact info, tax IDs) is regularly reviewed and updated. This minimizes the risk of misdirected payments and helps meet compliance standards.

Always perform a two-way or three-way match (invoice vs. purchase order and goods receipt). This verification step ensures that you’re only paying for goods and services received and prevents overpayments or duplicate payments.

Use automation tools to streamline invoice processing, approvals, and payment execution. Automation reduces manual errors, accelerates cycle times, and provides a clear audit trail.

Reconcile payment records against bank statements regularly, ideally, daily or weekly. This ensures errors or discrepancies are caught early, which supports accurate financial reporting and fraud prevention.

Protect banking and vendor data with strong access controls, encryption, and secure systems. Limit access to payment functions based on roles and responsibilities. Using AML software alongside these safeguards helps detect suspicious activity early and adds another layer of protection to sensitive financial data.

Have clear written procedures for how and when payments are processed. This promotes consistency, accountability, and faster onboarding for new finance team members.

Streamlining your payment process doesn’t have to be complicated. DepositFix makes it simple and efficient. DepositFix automates payment collection, tracking, and processing, and helps businesses eliminate manual work, reduce errors, and accelerate cash flow.

Whether you're managing one-time transactions or recurring payments, DepositFix integrates seamlessly with your existing tools, giving you full visibility and control over your revenue. With features like customizable payment forms, automated receipts, and real-time reporting, you can offer a smooth payment experience for customers while staying on top of your finances.

Optimize your payments with DepositFix and focus more on growing your business, not chasing invoices. Book your free demo and see how!

Running payments is more than just transferring funds, it’s a structured, strategic process that ensures your business meets its financial obligations accurately, securely, and on time.

Follow each step carefully, from receiving and validating invoices to scheduling, executing, and reconciling payments, so you can strengthen vendor relationships, maintain healthy cash flow, and reduce operational risks.

Applying best practices like centralized scheduling, automation, and dual authorization further enhances the reliability and efficiency of your payment cycle.

With the right tools and processes in place, your business can transform payment management from a manual task into a seamless, value-adding function.

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!