A merchant agreement is a legally binding contract between a business (the merchant) and a payment processor, acquiring bank, or merchant services provider. This agreement outlines the terms and conditions under which the merchant is authorized to accept and process credit card, debit card, and other forms of electronic payments. It typically includes details about processing fees, chargeback policies, settlement timelines, compliance requirements, and responsibilities of both parties.

For example, the agreement may specify the percentage or flat-rate fee charged for each transaction, monthly minimums, or penalties for non-compliance with standards like PCI-DSS (Payment Card Industry Data Security Standard). It also governs how disputes and chargebacks are handled, what types of transactions are allowed, and how long it takes for funds to be deposited into the merchant's account.

Reviewing this document carefully, and possibly consulting with legal or financial advisors, can help merchants avoid hidden fees and ensure they are meeting their obligations.

Most Important Parts of a Merchant Agreement

When reviewing a merchant agreement, you should understand its key components, as these terms directly impact how your business processes payments, handles disputes, and manages costs. A well-structured agreement should clearly define the roles, fees, and responsibilities involved. Here are the most important parts to pay close attention to:

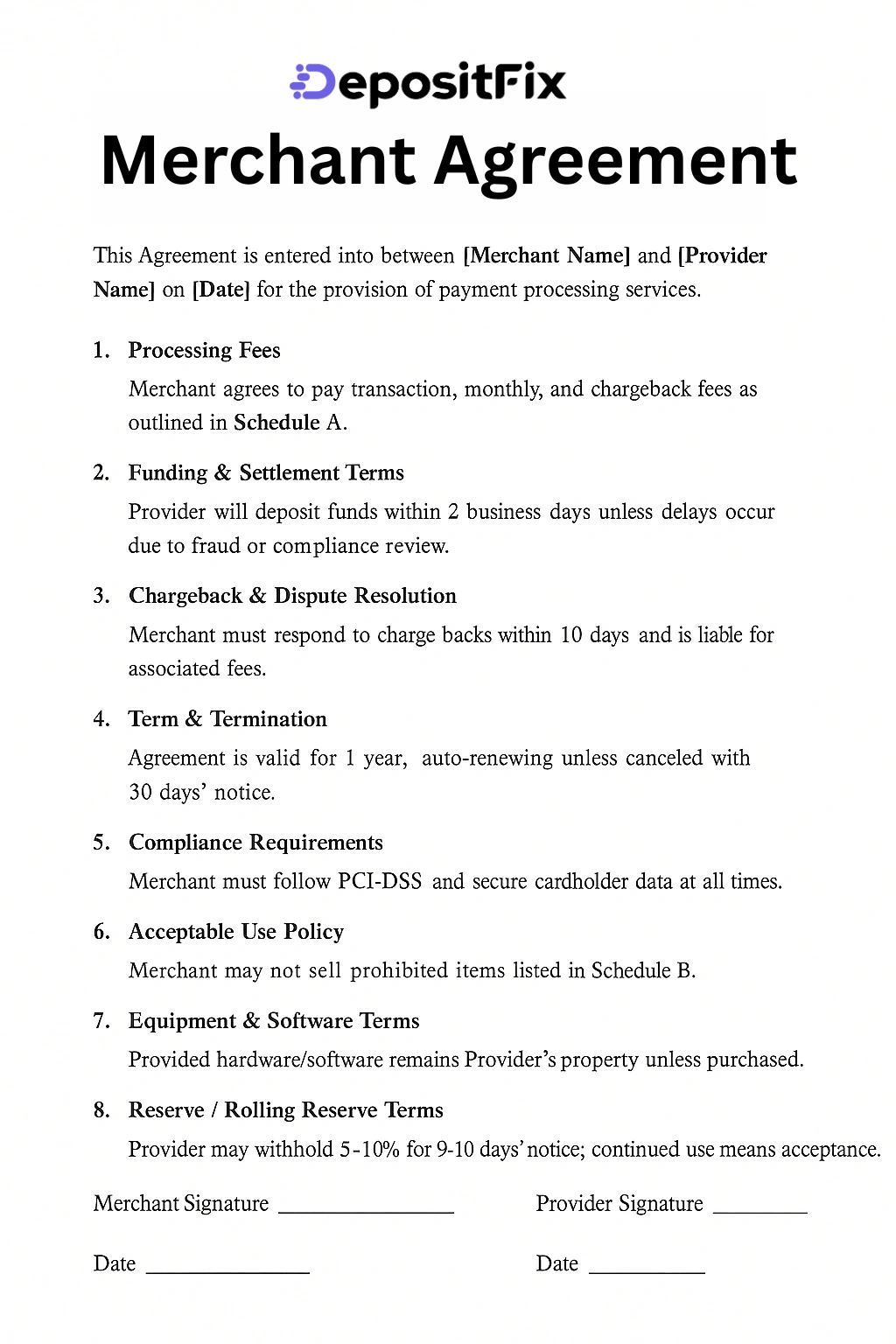

- Processing Fees: Includes transaction fees, monthly fees, chargeback fees, and other costs related to payment processing.

- Funding and Settlement Terms: Specifies how and when funds from processed transactions will be deposited into your account.

- Chargeback and Dispute Resolution: Outlines the process for handling chargebacks, including timelines, merchant responsibilities, and associated penalties.

- Term and Termination Clauses: Describes the duration of the agreement and the conditions under which either party can terminate the contract.

- Compliance Requirements: Includes obligations related to PCI-DSS compliance and any other industry regulations.

- Acceptable Use Policy: Defines the types of products or services you can sell under the agreement and what is prohibited.

- Equipment and Software Terms: Covers the use, lease, or purchase of terminals, POS systems, or payment gateways.

- Reserve or Rolling Reserve Requirements: Details if and how the provider will hold a percentage of funds to mitigate risk.

- Amendment and Fee Change Policy: Explains how and when the provider can change fees or terms, often with minimal notice.

What to Look Out for Before Signing a Merchant Agreement

Before signing a merchant agreement, carefully evaluate the fine print to avoid unexpected fees, restrictive terms, or long-term obligations that could negatively affect your business. Here’s what to look out for:

- Hidden Fees: Watch for fees not clearly disclosed, such as PCI non-compliance fees, statement fees, monthly minimums, batch fees, or early termination charges. Some providers advertise low rates but include hidden costs elsewhere in the contract.

- Termination Clauses and Contract Length: Many agreements lock you into long-term contracts with auto-renewal clauses and high early termination fees. Make sure you understand the contract duration, the process for cancellation, and any penalties.

- Rate Structure: Understand whether the provider uses a flat-rate, tiered, or interchange-plus pricing model. Some pricing structures can be confusing and more expensive in the long run, especially for small or seasonal businesses.

- Chargeback Policies: Review how chargebacks are handled, including response timeframes, your responsibilities, and related fees. Excessive chargeback penalties or unclear dispute resolution processes can lead to financial losses.

- Fund Holding and Reserve Terms: Some providers hold a percentage of your funds in a reserve account or delay settlements, especially for high-risk businesses. Understand the conditions that trigger these holds and how long funds are withheld.

- Fee Change Flexibility: Check whether the provider can raise fees or change terms without notice. Many agreements include clauses that give the provider the right to adjust pricing at any time.

- PCI Compliance Requirements: Confirm whether you're responsible for maintaining PCI compliance and if there are penalties for failing to meet those requirements. Some providers charge annual PCI compliance or non-compliance fees.

- Exclusivity or Bundling: Some agreements require you to exclusively use the provider for all payment processing or bundle unnecessary services (like leasing equipment), which can add unnecessary costs.

Read the full agreement, including the terms and conditions and any addendums. If anything seems unclear or overly complex, consider seeking legal or financial advice before signing.

Merchant services enable businesses to accept and manage secure electronic payments via card processing, POS systems, and online payment gateways.

A merchant account lets businesses accept card payments, holding funds temporarily before depositing them into the main business bank account.

A merchant statement summarizes all card transactions, fees, and deposits, helping businesses track sales, spot errors, and manage payment processing costs.

Ready to streamline your payment operations?

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!