A transaction fee is a charge that a business or individual incurs each time a financial transaction is processed, typically when a payment is made through a credit card, debit card, online payment gateway, or other electronic methods.

These fees are generally imposed by payment processors, acquiring banks, or credit card networks (like Visa, Mastercard, or American Express) as compensation for facilitating the transaction and ensuring its security.

Transaction fees can vary depending on several factors, such as the type of payment method used, the location of the transaction, the currency exchange involved (if any), and the risk associated with the transaction.

For example, online or card-not-present transactions usually come with higher fees due to the increased risk of fraud. In a typical merchant services setup, the transaction fee might include components like an interchange fee (paid to the card-issuing bank), a processor markup, and assessment fees from the card network. These fees can be structured as a flat fee, a percentage of the transaction amount, or a combination of both (e.g., 2.9% + $0.30 per transaction).

While transaction fees are often a small portion of each sale, they can significantly impact profit margins, especially for businesses with high volumes or low average transaction values.

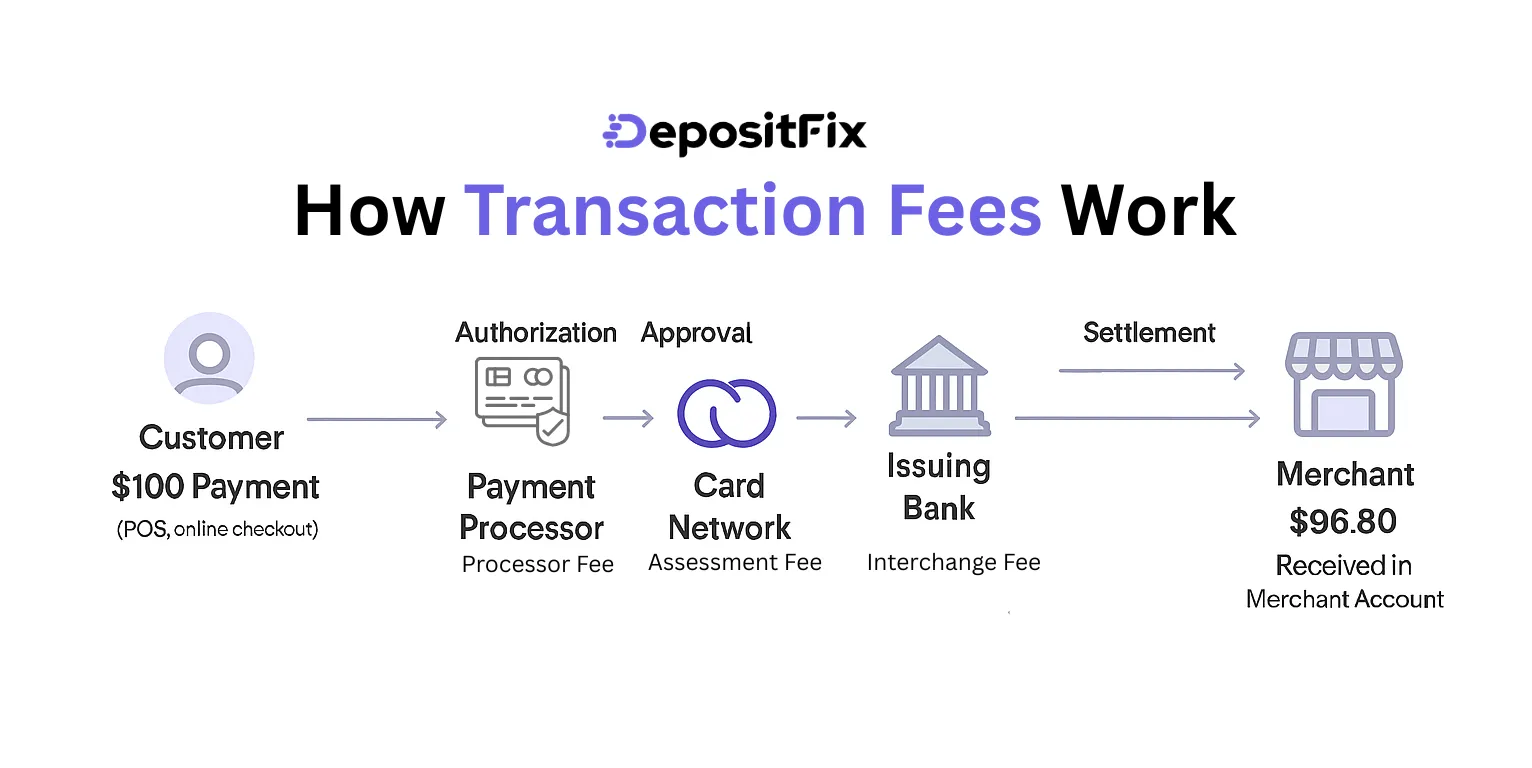

How Transaction Fees Work

When a customer makes a payment, whether online or in person, several parties are involved in processing that transaction, and each takes a small cut in the form of fees. Here's how it works in a typical card-based payment scenario:

- Customer Initiates the Payment: The process begins when a customer uses their credit or debit card to pay for a product or service. This could be through a physical point-of-sale (POS) terminal or an online checkout page.

- Payment Processor Steps In: The merchant’s payment processor routes the transaction details to the card network (such as Visa, Mastercard, or American Express), which then contacts the customer’s bank (called the issuing bank) to request authorization.

- Authorization and Approval: The issuing bank checks the customer’s account to ensure they have sufficient funds or credit, and then approves or declines the transaction. If approved, the bank places a hold on the funds.

- Transaction Completion and Settlement: Once approved, the merchant completes the sale. The funds (minus fees) are transferred to the merchant’s bank (called the acquiring bank) in a process known as settlement, usually within one to three business days.

- Fee Breakdown: During this process, fees are deducted and distributed among the involved parties:

- Interchange Fee: Paid to the issuing bank for handling the transaction and assuming the risk.

- Assessment Fee: Charged by the card network for using its infrastructure.

- Processor Fee: Charged by the payment processor for routing and managing the transaction.

- Final Payout: The merchant receives the payment amount minus all applicable fees. For example, if a customer pays $100 and the total transaction fee is 2.9% + $0.30, the merchant would receive $96.80

These fees can vary depending on the type of card used (debit vs. credit, rewards vs. standard), the merchant’s industry, transaction volume, and whether the card was physically present or entered online. Some businesses may negotiate lower fees based on their sales volume or choose different pricing models, like flat-rate, tiered, or interchange-plus pricing.

Factors that Influence Transaction Fees

Transaction fees aren’t one-size-fits-all, they vary based on a number of factors tied to the nature of the payment, the risk level, and the agreements between merchants and payment providers. Here are the key factors that influence how much a business pays per transaction:

- Payment Method Used: Different payment methods come with different fee structures. Credit cards typically have higher fees than debit cards due to greater fraud risk and credit underwriting. Similarly, digital wallets (like PayPal or Apple Pay) may include additional service fees on top of standard card processing fees.

- Card Type: The type of card a customer uses, standard, business, premium, or rewards card, can significantly affect the interchange fee. Premium and rewards cards generally carry higher fees because card issuers need to fund the cardholder perks and cashback incentives.

- Transaction Environment: Card-present transactions (e.g., in-store with chip or tap) usually have lower fees than card-not-present transactions (e.g., online or over the phone), which carry more risk of fraud and chargebacks. As a result, online businesses often face higher transaction fees.

- Merchant Industry and Risk Profile: Certain industries are considered higher risk by payment processors, such as travel, adult content, supplements, or subscription-based services. Merchants in these industries may be charged higher transaction fees due to a greater likelihood of chargebacks or fraud.

- Transaction Volume and Average Ticket Size: Businesses that process a high volume of transactions may be eligible for discounted rates from processors. Additionally, merchants with higher average transaction amounts might benefit from lower percentage fees or flat-rate structures.

- Processor Pricing Model: The pricing structure chosen by the merchant impacts how fees are applied. Common models include flat-rate pricing (e.g., 2.9% + $0.30), tiered pricing (grouped by transaction type), and interchange-plus pricing (interchange fee + processor markup). Each has its pros and cons depending on business size and payment behavior.

- Currency Conversion and Cross-Border Transactions: International payments often come with extra fees for currency conversion and cross-border processing. These added charges compensate for the additional risk and complexity of global transactions.

- Security and Compliance Level: Businesses that meet the highest security standards (e.g., PCI DSS compliance) and use fraud detection tools may benefit from lower fees, as they present lower risk to payment processors and card networks.

Understanding these influencing factors can help businesses take strategic steps to reduce costs, such as encouraging lower-fee payment methods, negotiating better processor terms, or enhancing payment security to minimize risk-related surcharges.

Types of Transaction Fees

Transaction fees come in several forms, depending on the payment method, the parties involved, and how the transaction is processed. Here are the most common types of transaction fees that businesses may encounter when accepting payments:

- Interchange Fees: This is the largest component of most transaction fees. It’s paid by the merchant’s bank (acquiring bank) to the customer’s bank (issuing bank) and is set by card networks like Visa and Mastercard. Interchange fees typically include a percentage of the transaction amount plus a fixed fee, and they vary based on card type, payment method, transaction risk, and merchant category.

- Assessment Fees: These are fees charged by the card networks (e.g., Visa, Mastercard, American Express) for using their infrastructure and brand. Assessment fees are typically lower than interchange fees and are calculated as a small percentage of the transaction volume.

- Payment Processor Fees: Payment processors charge merchants for handling the technical aspects of the transaction, such as communicating with banks and card networks. This fee often includes customer support, fraud prevention tools, and reporting features. It can be structured as a flat fee, a percentage, or part of a bundled pricing model.

- Flat Per-Transaction Fees: Some pricing models include a fixed fee per transaction, often seen in flat-rate structures like "2.9% + $0.30." The flat fee portion helps cover the base cost of processing each individual transaction.

- Gateway Fees: If a merchant uses a third-party payment gateway to securely transmit payment data (especially in online transactions), an additional gateway fee may apply. This fee can be monthly or per transaction, depending on the provider.

- Monthly or Annual Fees: Some payment providers charge ongoing fees for account maintenance, access to premium features, PCI compliance, or customer support. While not tied to a single transaction, they contribute to the overall cost of payment processing.

- Chargeback Fees: When a customer disputes a charge and files a chargeback, the merchant may be charged a fee regardless of whether the dispute is resolved in their favor. These fees are meant to discourage excessive disputes and cover administrative costs.

- Cross-Border Fees: If a payment involves multiple currencies or banks located in different countries, cross-border fees may apply. These are designed to account for additional risk, currency conversion, and international processing costs.

- Batch Fees: At the end of each business day, merchants "batch" or settle all completed transactions to receive payment. Some providers charge a small fee per batch settlement.

- Early Termination or Contract Fees: Though not a per-transaction charge, some payment providers include penalties for breaking long-term contracts or switching services before the agreed period ends.

A chargeback is a transaction reversal initiated by a customer disputing a card charge to recover funds from the merchant through their bank or card issuer.

A surcharge fee is an extra charge businesses add to cover credit card processing costs, helping merchants offset fees and protect profit margins.

Ready to streamline your payment operations?

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!