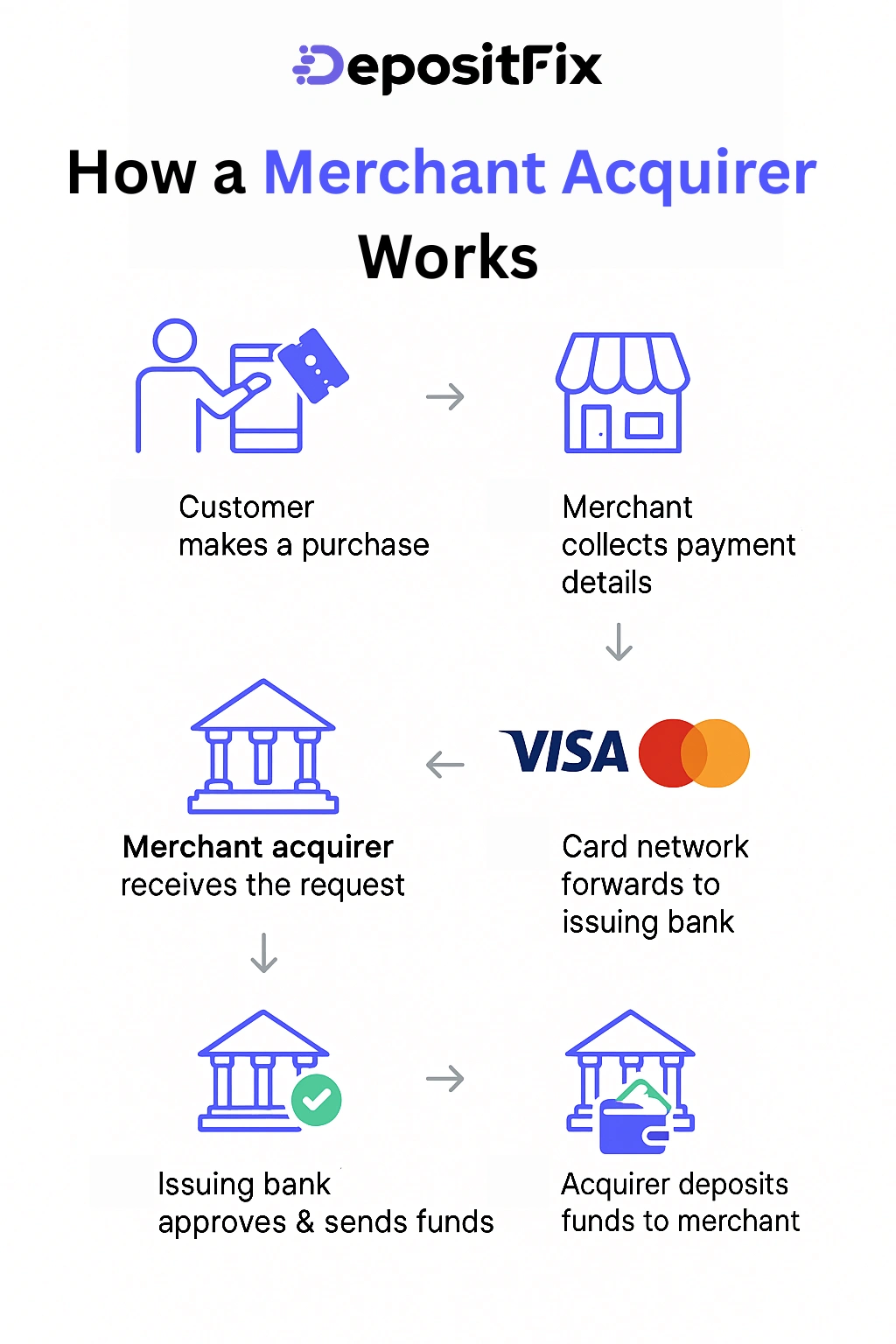

A merchant acquirer, also known simply as an acquirer or acquiring bank, is a financial institution or bank that processes credit and debit card payments on behalf of a merchant. It acts as an intermediary between the merchant and the cardholder's bank (known as the issuing bank) to facilitate electronic payment transactions.

When a customer uses a card to make a purchase, the merchant acquirer receives the transaction details, routes them through the card networks (like Visa, Mastercard, or American Express), and communicates with the issuing bank to authorize the transaction. Once approved, the acquirer ensures that the funds are transferred to the merchant’s account, minus processing fees.

Merchant acquirers also provide merchants with the tools and services needed to accept card payments, including point-of-sale (POS) systems, payment gateways for online transactions, fraud prevention tools, and compliance support for security standards like PCI DSS.

What Does a Merchant Acquirer Do

A merchant acquirer enables businesses to accept card-based transactions and manages the flow of funds between customers and merchants. Their responsibilities include a wide range of technical, financial, and compliance-related services that support both in-store and online payment environments. Key functions of a merchant acquirer include:

- Transaction processing: Routes payment information from the merchant to the card networks and issuing banks for authorization.

- Settlement and funding: Transfers approved funds from the customer’s bank to the merchant’s account, typically after deducting processing fees.

- Merchant account services: Provides and manages the merchant account where card payments are temporarily held before being deposited.

- Fraud prevention and risk management: Monitors transactions for suspicious activity and helps protect against chargebacks and fraud.

- Compliance support: Ensures the merchant adheres to industry regulations such as PCI DSS for secure handling of cardholder data.

- Technology and integration: Supplies POS terminals, online payment gateways, and reporting tools to streamline operations and track transactions.

Merchant Acquirer vs Payment Processor

The difference between a merchant acquirer and a payment processor lies in their roles within the payment ecosystem, though they often work closely together and are sometimes offered by the same provider.

A merchant acquirer (or acquiring bank) is a financial institution that enables businesses to accept card payments. It provides the merchant account where funds are deposited after a successful transaction and is responsible for settling transactions, transferring funds from the issuing bank to the merchant, and ensuring compliance with security standards like PCI DSS. Acquirers also assume financial risk for each transaction, such as chargebacks or fraudulent activity.

On the other hand, a payment processor is a technology provider that handles the technical side of moving transaction data between all parties involved in a payment. It connects the merchant, the acquirer, the card network (like Visa or Mastercard), and the issuing bank. The processor routes authorization requests, transmits transaction details, and ensures payments are approved or declined in real time. It may also provide tools like payment gateways, POS software, and fraud detection systems.

In short:

- The merchant acquirer manages the financial side of the transaction and holds the merchant account.

- The payment processor manages the technical flow of the transaction data between parties.

In many cases, these roles are bundled together, but the distinction is important when dealing with traditional banks or enterprise-level setups.

Who Needs a Merchant Acquirer

Any business that wants to accept credit card, debit card, or digital wallet payments from customers needs a merchant acquirer. This includes both brick-and-mortar stores and online businesses, as well as service providers and subscription-based platforms. Any organization that processes card payments needs a merchant acquirer to facilitate those transactions and receive the funds securely. Specific examples of who needs a merchant acquirer include:

- Retail stores: To accept in-person card payments via point-of-sale (POS) systems.

- E-commerce businesses: To process online transactions through payment gateways.

- Restaurants and cafes: For quick, secure card and mobile payments.

- Healthcare providers: To collect payments from patients through terminals or billing systems.

- Professional service firms: Such as law firms or consultants who accept card payments for services rendered.

- Subscription businesses: For recurring billing and automated payment collection.

Without a merchant acquirer, a business cannot obtain a merchant account or settle card transactions.

Merchant services enable businesses to accept and manage secure electronic payments via card processing, POS systems, and online payment gateways.

A merchant account lets businesses accept card payments, holding funds temporarily before depositing them into the main business bank account.

Ready to streamline your payment operations?

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!