Credit card processing without monthly fees is a cost-effective solution for small businesses and independent merchants looking to accept card payments without the burden of fixed charges.

Unlike traditional processors that charge a monthly service or statement fee, these providers only collect fees when you actually process a transaction.

This pay-as-you-go model can significantly reduce overhead costs and make it easier to manage cash flow, especially for seasonal businesses or those just starting out.

Zero fee credit card processing is a pricing model where businesses pass the cost of credit card transaction fees directly to their customers, allowing the business to effectively pay nothing for card processing.

Instead of absorbing the typical 2%–4% processing fee charged by payment processors, the business adds a small surcharge to the customer’s bill when a credit card is used. This model is often implemented using compliant surcharging programs or cash discount programs, both of which must follow strict regulations, especially for Visa, Mastercard, and state-specific laws.

Zero fee processing can be an attractive option for small businesses and service providers looking to maximize revenue and reduce operational costs, but it’s important to disclose the surcharge clearly to customers at the point of sale and on receipts. While it helps protect profit margins, businesses should consider customer perceptions and potential pushback, especially in competitive markets where pricing sensitivity is high.

Credit card processing without monthly fees follows a pay-as-you-go model, where businesses only incur charges when they process a transaction. This setup is ideal for small, new, or seasonal businesses that want to avoid the burden of fixed monthly costs. Here's how it typically works:

This model offers flexibility and cost control, especially for low-volume businesses. However, review the processor’s fee schedule, as some may charge higher per-transaction rates or hidden service fees to offset the lack of monthly charges.

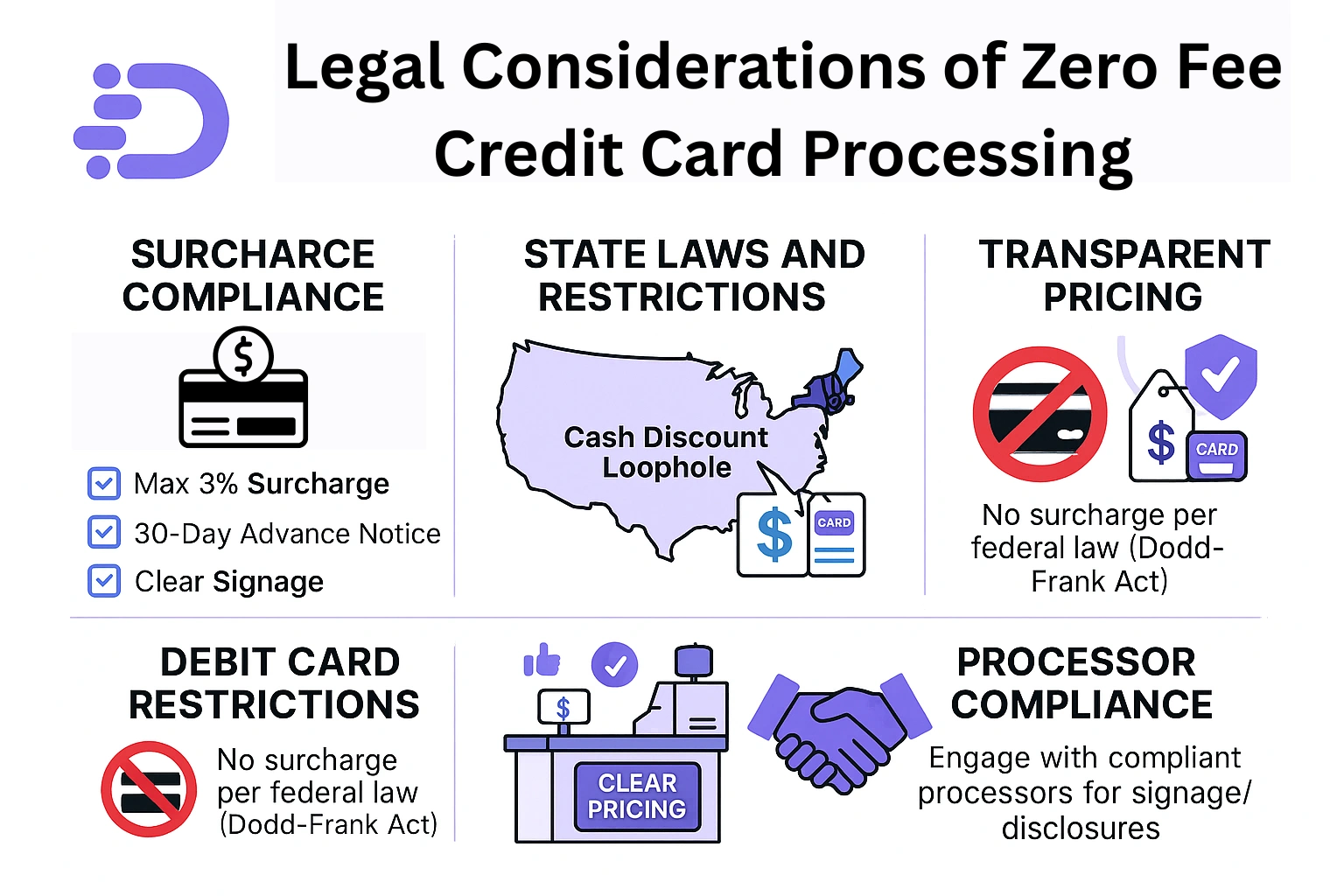

Here are some important legal considerations businesses must keep in mind when implementing zero fee credit card processing:

To legally pass credit card fees to your customers, you must follow specific rules set by the major card networks.

Your ability to add credit card surcharges may be limited depending on where your business operates.

No Surcharges on Debit Transactions: Even if a debit card is run “as credit,” surcharges are not allowed under federal law (Dodd-Frank Act).

Surprises at checkout can damage trust, lead to chargebacks, or result in legal complaints.

Work with a payment processor that offers a compliant zero-fee or surcharge program. They should guide you through proper disclosure, signage, and reporting requirements.

While free credit card processors can be appealing, look beyond the absence of monthly fees and carefully evaluate the full offering, including any potential hidden costs or limitations.

One of the most important factors is clear and upfront pricing. The processor should openly disclose all transaction fees, surcharges, and any other charges associated with using their service. Ideally, you want a simple, flat-rate pricing structure, such as a fixed percentage plus a small fee per transaction, to avoid surprises. Be cautious of providers that use vague pricing terms or hide fees in the fine print, as this can lead to unexpected costs down the line.

Even if the processor advertises no monthly fees, some may charge additional fees for things like PCI compliance, chargebacks, hardware rentals, or inactivity. Carefully review the terms and conditions to identify any such hidden or conditional fees. Additionally, check if there are minimum processing volume requirements that you must meet to avoid penalties or additional charges.

Look for processors that offer multiple support channels such as live chat, phone, or email, and pay attention to their hours of availability. Reading user reviews can give valuable insight into how responsive and helpful their support team is, which can be a major factor if you encounter technical or payment issues.

Some processors might lock you into long-term contracts or impose early termination fees, even if they advertise as “free.” It’s preferable to choose providers that offer month-to-month agreements with no cancellation penalties, giving you the flexibility to switch if the service doesn’t meet your expectations. Always ask about any commitments or minimum usage clauses before signing up.

Free credit card processors often restrict access to advanced tools or integrations unless you pay for a premium plan. Verify which features, such as invoicing, virtual terminals, or reporting dashboards, are included at no cost. Consider whether the platform has the functionality to support your business as it grows, or if you’ll be forced to upgrade sooner than expected.

If the processor offers a zero-fee or surcharge model, they should provide guidance and tools to keep your business compliant with card network rules and applicable state laws. This includes providing clear signage, customer disclosures, and training materials to ensure proper communication of fees. Also, confirm how the processor differentiates between credit and debit card payments to avoid unintentional violations.

DepositFix offers businesses credit card processing with $0 monthly fees, making it an excellent choice for merchants who want to avoid fixed costs and pay only when they process payments. This pay-as-you-go model means you’re charged solely on a per-transaction basis, helping startups, small businesses, and seasonal sellers reduce overhead and manage expenses efficiently.

With DepositFix, businesses benefit from a cost-effective, transparent, and scalable credit card processing solution, allowing you to focus on growth without worrying about monthly fees or hidden charges.

Credit card processing without monthly fees is a flexible and affordable payment solution tailored to the needs of small businesses, startups, and seasonal sellers. When merchants adopt a pay-as-you-go model, they can eliminate fixed costs and only pay when they process transactions, making cash flow management easier and more predictable.

Zero fee credit card processing, where fees are passed to customers via compliant surcharging or cash discount programs, offers another way to reduce expenses, but requires careful attention to legal requirements and transparent communication.

When choosing a free or no-monthly-fee processor, look beyond just the absence of monthly charges and consider factors like transparent pricing, customer support, contract terms, and feature availability to avoid hidden costs and limitations.

Solutions like DepositFix exemplify how businesses can enjoy $0 monthly fees while accessing user-friendly tools, PCI compliance, and flexible payment options, helping merchants focus on growth without the burden of unexpected fees.

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!