An acquirer, or acquiring bank, works directly with merchants to process card payments, ensuring funds flow from customers to businesses smoothly. An issuer, on the other hand, is the bank that provides the customer with a credit or debit card, manages their account, and approves or declines transactions.

What Is an Acquirer

An acquirer, often referred to as an acquiring bank or merchant bank, is a financial institution that processes credit and debit card payments on behalf of a merchant. The acquirer acts as the intermediary between the merchant and the card networks, such as Visa or Mastercard.

When a customer makes a purchase using a card, the acquirer receives the transaction details from the merchant, routes them to the card network, and then communicates with the customer’s issuing bank to authorize the payment. Once authorized, the acquirer ensures that the funds are transferred from the cardholder’s bank account to the merchant’s account, typically minus any processing fees.

Beyond transaction processing, acquirers also manage risk, handle chargebacks, and ensure that merchants comply with industry standards such as PCI DSS. They often provide additional services, including merchant accounts, fraud detection tools, and reporting dashboards that help businesses monitor sales and manage payments efficiently.

For merchants, partnering with a reliable acquirer guarantees smooth transaction processing and provides the trust and security necessary to handle sensitive cardholder data, reduce financial risk, and maintain seamless operations in today’s increasingly digital commerce landscape.

What Is an Issuer

An issuer, also known as an issuing bank or card issuer, is a financial institution that provides payment cards, such as credit cards, debit cards, or prepaid cards, to consumers and businesses.

The issuer is responsible for managing the cardholder’s account, setting credit limits, monitoring transactions, and billing for purchases made using the card. When a cardholder initiates a payment, the issuer authorizes or declines the transaction based on factors such as available funds, creditworthiness, and potential fraud detection alerts.

Beyond processing payments, issuers often offer rewards programs, cashback incentives, and other benefits to encourage card usage. They also play a role in security, employing technologies like EMV chips, tokenization, and real-time fraud monitoring to protect both cardholders and merchants.

In the broader payment ecosystem, the issuer works closely with card networks, which route transaction information between the issuer and the acquiring bank. Issuers extend credit or provide access to funds, and enable consumers to make purchases conveniently while assuming a degree of financial risk, which they manage through account monitoring, interest charges, and payment terms.

For cardholders, a reliable issuer ensures access to secure payment methods, seamless transactions, and support in case of disputes, making it a cornerstone of the modern cashless economy.

What Is the Difference Between an Acquirer and Issuer

An acquirer, or acquiring bank, works with merchants to process card payments. It receives transaction details from a merchant, forwards them through the card network, and ultimately ensures that funds are transferred to the merchant’s account once the payment is approved.

The issuer, or issuing bank, is the financial institution that provides the customer with a credit or debit card and manages the cardholder’s account. When a cardholder makes a purchase, the issuer evaluates the transaction, checks for available funds or credit, and either approves or declines the payment.

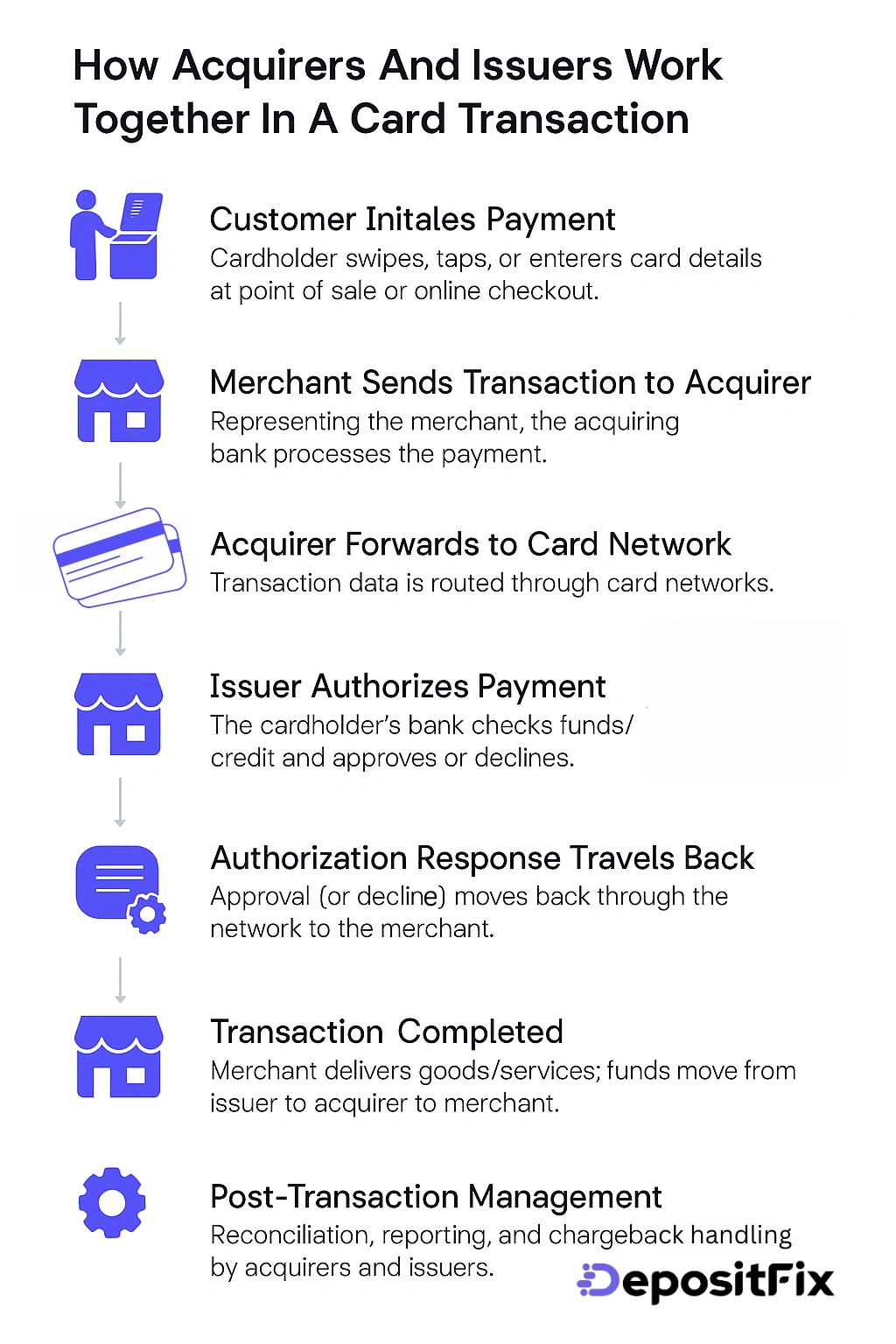

How Acquirers and Issuers Work Together in a Card Transaction

- Customer Initiates Payment – The cardholder swipes, taps, or enters their card details at a merchant’s point of sale or online checkout.

- Merchant Sends Transaction to Acquirer – The merchant’s bank (the acquirer) receives the payment information and prepares it for authorization.

- Acquirer Forwards to Card Network – The acquirer sends the transaction data to the card network (Visa, Mastercard, etc.), which routes it to the cardholder’s issuer.

- Issuer Authorizes Payment – The issuer checks the cardholder’s account for available funds or credit, reviews fraud alerts, and approves or declines the transaction.

- Authorization Response Travels Back – The issuer sends the approval or decline back through the card network to the acquirer, which relays it to the merchant.

- Transaction Completed – If approved, the merchant provides the goods or services. The issuer transfers funds to the acquirer, who deposits them into the merchant’s account (minus processing fees).

- Post-Transaction Management – Both acquirers and issuers handle reconciliation, reporting, and potential chargebacks to ensure security and accuracy.

A merchant acquirer processes card payments, connects merchants to card networks, and ensures secure fund transfers from customers to businesses.

Ready to streamline your payment operations?

Discover the hidden automation in your payment, billing and invoicing workflows. Talk to our experts for a free assement!